{kind=link}

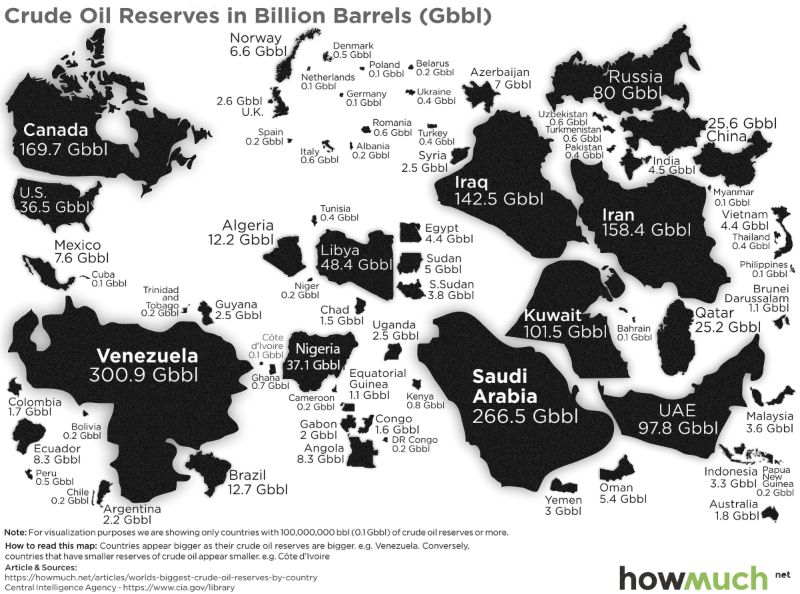

Nigeria sits on an estimated 37.1 billion barrels of proven oil reserves—more than the UK (2.6 billion) and Norway (6.6 billion) combined. Yet Nigeria, Africa’s largest oil producer, has for decades imported most of its gasoline.

At first glance, this sounds like an economic absurdity. On closer inspection, it exposes something more structural—and more uncomfortable—about the global energy system and Africa’s place within it.

Nigeria exports crude oil to Europe.

Europe refines it.

Nigeria buys it back as gasoline—often at many times the original value.

This is not a uniquely Nigerian problem. It is a continental pattern.

Libya: ~48.4 billion barrels of oil reserves. Imports diesel.

Angola: ~8.3 billion barrels. Imports refined fuel.

Algeria: ~12.2 billion barrels. Imports refined petroleum products.

Africa has the oil.

Europe has the refineries.

Africa exports raw materials.

Europe captures value.

That pattern should sound familiar.

The Refining Gap Is Not an Accident

Oil wealth does not come from crude alone. It comes from processing, refining, petrochemicals, logistics, and downstream industries—the parts of the value chain where margins are highest and jobs are most durable.

For decades, African countries have been locked out of that value chain.

This has often been explained away with technical arguments:

“Refineries are too expensive.”

“Local demand is insufficient.”

“Governance risks scare off investors.”

“It’s more efficient to import refined products.”

But efficiency for whom?

European and global oil companies have built sprawling refining networks, backed by export credit agencies, development banks, and state guarantees. African refineries, by contrast, have faced a maze of financing hurdles, regulatory pressures, sanctions risk, technology restrictions, and shifting international ‘standards’—often imposed by the very same countries that buy Africa’s crude.

When African states try to move downstream, obstacles multiply:

Financing suddenly becomes “too risky.”

Technology transfers get delayed or restricted.

Environmental and compliance standards rise overnight.

International partners develop “concerns.”

None of these challenges are imaginary. But neither are they neutral.

The Dangote Effect

The Dangote Refinery in Nigeria, with a capacity of 650,000 barrels per day, is the largest refinery in Africa and one of the largest in the world. Its opening has already begun to reshape Nigeria’s fuel import equation and regional energy flows.

One refinery—just one—has started to:

Reduce gasoline imports

Save billions in foreign exchange

Create thousands of direct and indirect jobs

Anchor a domestic petrochemical industry

If a single facility can do this, the implication is obvious: the old system was not inevitable. It was maintained.

For years, Nigeria was told refining locally did not make economic sense. The moment it became reality, the narrative changed to concerns about pricing, competition, and “market distortions.”

Conveniently late concerns.

Colonialism, Rebranded

Calling this “colonialism” makes some audiences uncomfortable. But strip away the emotion and look at the structure:

Raw materials flow from Africa to Europe.

Value-added processing happens elsewhere.

Finished products return to Africa at a premium.

Capital accumulates in the Global North.

Dependency is preserved in the Global South.

This is not classical colonialism with flags and governors. It is industrial colonialism, enforced through supply chains, finance, trade rules, and “best practices.”

The language has changed. The power dynamics have not.

Western governments frequently speak about “African development,” “industrialisation,” and “value addition.” Yet when African countries attempt precisely that—especially in strategic sectors like energy—the response is rarely enthusiastic support.

Development is encouraged in theory, constrained in practice.

The Cost of Dependency

For Nigeria, fuel imports have meant:

Chronic foreign exchange pressure

Fuel subsidies that hollow out public finances

Exposure to global price shocks

Lost industrial jobs and technical skills

For Africa more broadly, it has meant:

Missed opportunities for regional energy integration

Weak manufacturing bases

Continued vulnerability to external markets

The paradox of energy-rich countries facing energy poverty

This is not just an economic issue. It is a sovereignty issue. No country is truly independent if it cannot process its own resources.

Why This Matters Now

The global energy transition is accelerating. Fossil fuels will not disappear overnight, but the long-term trajectory is clear. The countries that control processing, technology, and industrial ecosystems will manage the transition on their own terms.

If African nations remain locked into raw-material export roles, they risk repeating the same dependency cycle in lithium, cobalt, rare earths, and green hydrogen.

Oil is not just about oil. It is about who controls value chains.

The Uncomfortable Question

Nigeria🇳🇬can refine its oil.

Angola🇦🇴can refine its oil.

Libya🇱🇾can refine its oil.

The issue has never been technical capacity. It has been political economy.

There is a very profitable global arrangement built on Africa exporting raw materials and importing finished products. Disrupting it threatens entrenched interests—from multinational corporations to financial institutions to states that benefit quietly from the status quo.

So the real question is not why Africa hasn’t industrialised faster.

The question is: who benefits when it doesn’t?

Until that question is confronted honestly, Africa will continue to sit atop vast wealth while paying a premium to access it.

Change the structure, and the outcomes will change too.