If you still think mobile money is a fintech product, you are misreading Africa.

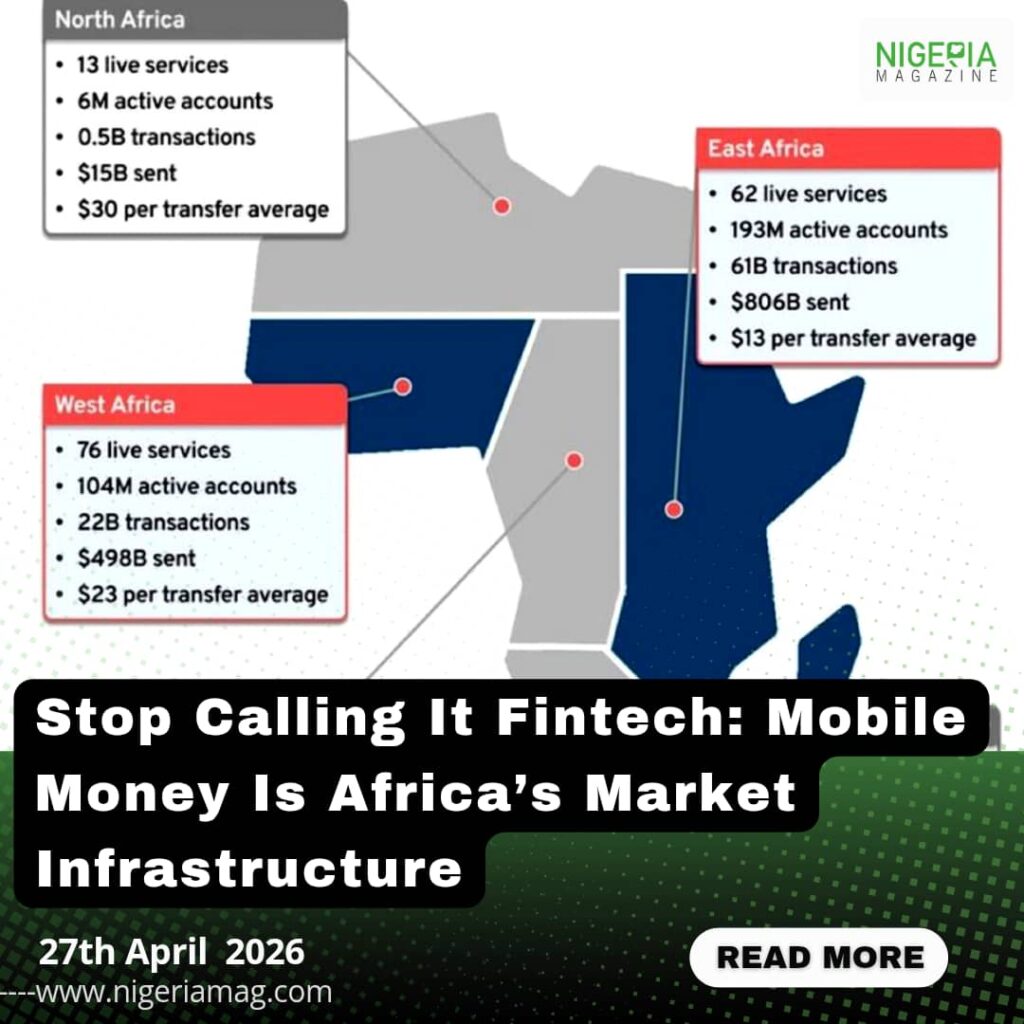

The Scale: In 2025, two regions moved over $1.3 trillion through phones.

→ East Africa: $806B

→ West Africa: $498B

This is not a payments trend. This is market infrastructure.

What makes it powerful:

Low transaction size: Daily purchases, not just large transfers

Very high frequency: Multiple transactions per user, per day

Deep daily use: Embedded in how people actually live

Food. Transport. Bills. Trade. The phone became the rail.

Where banking was too thin, too slow, or too far, mobile money became the system. It didn’t disrupt banks; it bypassed the need to wait for them.

The Market Reality:

If people cannot pay you through mobile money, you are not in the market. Period.

This is true for a market trader in Kampala, a logistics SME in Lagos, or a pan-African e-commerce platform. Cash is fading. Cards never scaled. Mobile money won because it matched the rhythm of African life: small, frequent, trusted, instant.

Africa did not wait for banking to scale. It built a faster rail.

And it is already running.

For founders, investors, and policymakers: the question isn’t “Should we integrate mobile money?” The question is “Why aren’t you on the rail yet?”