{kind=link}

Moderating Growth, Persistent Risks

Global economic growth in 2026 is projected to remain modest, extending a post‑pandemic pattern of subdued expansion. According to the United Nations’ World Economic Situation and Prospects report, world GDP is forecast to grow by about 2.7% in 2026, slightly below 2025’s outcome and still beneath the pre‑COVID average of around 3.2%. (Reuters)

This slower pace reflects a mix of structural headwinds — mounting trade barriers, geopolitical uncertainty, and fragmented supply chains — alongside demand softening in key consumer economies. Advanced economies such as the United States and the Euro Area are expected to expand at modest rates, while China’s growth is decelerating from its historical highs. (Reuters)

Inflation Trends: On a Downward Path, But Uneven

Across major economies, inflation continues to cool from the peaks seen in the early 2020s. Central banks have achieved significant de‑risking of price pressures, but inflation remains above target in several large markets, especially the U.S., due to lingering tariff effects and supply constraints. (Reuters)

Emerging markets are also seeing gradual disinflation, although the pace varies.

Commodity price swings — particularly in energy and food — still influence price levels, keeping inflation trending above ideal central‑bank targets in many developing economies. (EY)

Interest Rates: Easing but With Caution

The policy stance of major central banks is gradually shifting from aggressive tightening to more accommodative postures. In the United States, forecasts indicate headline policy rates may edge lower in 2026 as inflation shows signs of settling, though they are likely to remain above pre‑pandemic norms. (AP News)

This anticipated shift — with lower short‑term rates and potentially softer long‑term yields — could ease external financing conditions for emerging markets. However, the sequencing and timing remain uncertain, meaning volatility in global capital flows could persist.

Emerging Markets: A Mixed Story

Emerging economies, including those in Sub‑Saharan Africa, China, and Latin America, are expected to outperform advanced economies in aggregate, albeit on a slowing trajectory. Growth estimates cluster around 3.5–4.0%, constrained by weaker global trade, financing challenges, and localized structural barriers. (Capital Economics)

Capital flows into emerging markets may benefit from a weaker U.S. dollar and lower global rates, improving asset returns and FX stability in some regions. (ING Think)

What This Means for Nigeria: Oil, Trade, FX, Inflation & Interest Rates

- Nigeria’s Oil Sector: Critical External Earnings Anchor

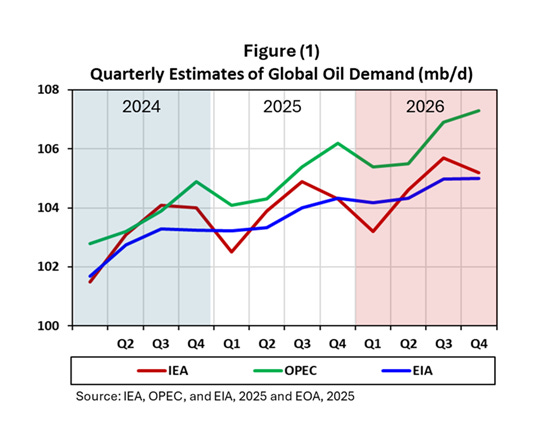

Oil remains Nigeria’s most important source of foreign exchange, fiscal revenue, and export earnings. Global oil demand growth in 2026 is expected to face significant headwinds — slower industrial activity in some regions and an accelerating energy transition to renewables are tempering crude consumption growth. (Industry commentary suggests demand growth is slowing from historical averages. (Reddit))

For Nigeria, this environment underscores the importance of output stability and diversification of production. Local forecasts, including from Fitch Solutions and CBN sources, suggest crude production could rise moderately in 2026 — but gains are modest compared with pre‑pandemic capacity due to ongoing infrastructure constraints. (ThisDayLive)

A price environment where Brent hovers near or below Nigeria’s fiscal breakeven (frequently cited near $55–$60 per barrel) will keep public finance under pressure, constraining spending and FX inflows. External earnings from gas exports and refined products — especially from strategic facilities like the Dangote refinery — will therefore be vital.

- Trade Outlook: Slight Growth, But Barriers Loom

Global merchandise trade is forecast to expand more slowly than overall GDP, restrained by tariff barriers and a general drift toward protectionism. (Tekedia)

For Nigeria, this slower global trade growth means constraints on export diversification beyond hydrocarbons and could slow the rebound of non‑oil exports. Regional trade integration efforts (e.g., within ECOWAS) remain important — but logistical bottlenecks and border frictions continue to hamper diversification.

- Inflation Trends: Disinflation Helps, But Risks Remain

Domestic inflation in Nigeria is set to continue easing in 2026, a trend reflected in official forecasts. The Central Bank of Nigeria (CBN) projects headline inflation to slow to around 12.9% — a marked improvement from multi‑year highs seen in 2024–2025. (Central Bank of Nigeria)

Lower global commodity prices and tighter coordination between fiscal and monetary authorities are key drivers of this disinflation. Yet imported inflation remains a risk: shifts in global energy costs, exchange rate volatility, or renewed supply shocks can quickly reverse gradual gains.

- Interest Rates: Softening to Support Growth

Nigeria’s monetary policy cycle appears to be transitioning. After years of high policy rates aimed at containing inflation, there is increasing room for rate easing in 2026 as price pressures moderate. Expectations from several analysts suggest continued rate reductions could support credit growth and investment — a welcome shift for businesses and consumers alike. (Premium Times Nigeria)

Still, the pace of cuts must be calibrated carefully. Too rapid a reduction could reignite inflation or weaken the naira, while too slow a pace could discourage private sector lending and domestic investment.

- FX Outlook: Stability With Vulnerabilities

Foreign exchange stability is crucial for Nigeria’s macroeconomic health — impacting trade costs, investment decisions, and inflation. The naira has shown signs of stabilization in early 2026, supported by central bank reforms and improvements in external reserves. (Business Post Nigeria)

However, this stability is fragile. Global rate shifts, oil price swings, and speculative FX flows can all exert pressure. If global monetary easing boosts carry trades into emerging markets, Nigeria could benefit from portfolio inflows that support the naira. But in adverse scenarios — especially if oil prices slump or external demand weakens — FX volatility could re‑emerge.

Strategic Implications for Nigeria

Economic Policy and Fiscal Planning

Strengthen fiscal buffers: Diversify revenue away from oil by expanding tax base and improving compliance.

Enhance export diversification: Invest in non‑oil export sectors (agriculture, manufacturing, services) to cushion shocks from oil price fluctuations.

Prudent debt management: Manage external and domestic debt carefully to avoid FX liabilities crowding out productive spending.

Monetary and FX Policies

Calibrated interest rate easing: Gradually lower rates as inflation stabilises to support growth without triggering new price pressures.

FX market depth: Continue reforms that improve FX liquidity and reduce speculative spikes in the naira.

Private Sector and Investment Climate

Boost investor confidence: Clear policy frameworks and transparent regulatory regimes will be essential to attract capital.

Leverage regional trade: Strengthen Nigeria’s position within West African and broader African markets through trade facilitation.

In 2026, the global economy enters a phase of calibrated moderation, with slower growth, steady disinflation, and a tentative shift toward looser monetary conditions in key economies.

For Nigeria, this global backdrop presents a mix of opportunities and risks. The outlook for the oil sector, external trade, inflation, and FX stability will be central to national economic performance — determining whether growth can be expanded beyond hydrocarbons and leveraged into broader socio‑economic gains.

Nigeria’s economy is expected to outperform the global average in 2026, but policy coherence, structural reforms, and effective macroeconomic management will be decisive. The interplay between global trends and domestic economic strategy will define whether 2026 becomes a year of sustainable recovery — or a missed opportunity amid shifting global dynamics.